Ce blog est personnel, la rédaction n’est pas à l’origine de ses contenus.

Introduction

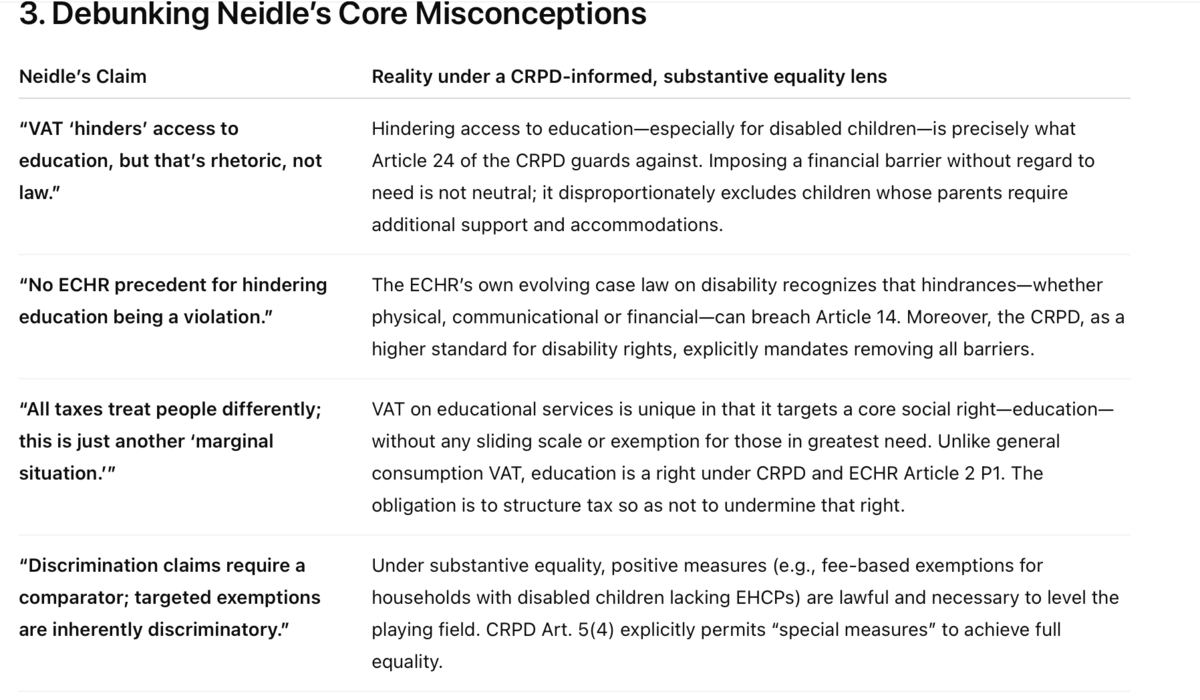

Dan Neidle’s recent analysis of the judicial review challenge to VAT on private school fees focuses narrowly on traditional tax and ECHR jurisprudence, overlooking both the systemic bias of ableism and the robust, rights-based framework established by the UN Convention on the Rights of Persons with Disabilities (CRPD). In doing so, it fails to recognise that tax policy interacts profoundly with disabled children’s rights to education, equality and inclusion. This article debunks the principal misconceptions in Neidle’s piece by:

Grounding the debate in the social and human rights–based model of disability, rather than the outdated “medical” or “charity” models he implicitly uses.

Demonstrating why a formal equality approach (treating everyone the same) is insufficient, and why substantive equality (addressing historical and systemic disadvantage) is essential—an approach endorsed by both the CRPD Committee and, increasingly, the European Court of Human Rights (ECHR).

Showing how the VAT measure, by disproportionately burdening families of disabled children (especially those without an EHCP), violates core CRPD principles and indeed risks contravening Article 14 (non-discrimination) and Article 24 (education) of the Convention.

1. Ableism and the Human Rights–Based Disability Model

Ableism refers to the pervasive social prejudice that devalues and limits the lives of people with disabilities, assuming that they must be “fixed” or accommodated only as a matter of charity. Neidle’s analysis—by treating special educational needs (SEN) as a peripheral “practical difficulty” and focusing on abstract tax doctrines—perpetuates this bias, rather than confronting how structural barriers (including tax burdens) exclude disabled children from meaningful participation.

By contrast, the human rights–based disability model, enshrined in the CRPD, recognises that:

Disability arises from the interaction between impairments and environmental attitudinal, legal or infrastructural barriers.

States have positive obligations to remove these barriers and to facilitate full inclusion (CRPD Art. 9: Accessibility; Art. 24: Education).

Non-discrimination is substantive: it demands not merely neutrality but affirmative measures to achieve genuine equality (CRPD Art. 5(4)).

Neidle cites the absence of EHCPs or other special arrangements as though the lack of an EHCP is merely an individual failing, rather than evidence of systemic under-provision. Under the CRPD, failure to identify and support children with SEN through state schools is itself a breach of the right to education—so burdening those families with additional VAT intensifies multiple layers of exclusion.

2. Beyond Formal Equality: The Case for Substantive Equality

2.1 Formal vs Substantive Equality

Formal equality insists that a law is non-discriminatory so long as it applies identically to everyone. Under this lens, taxing all private school fees at 20 % appears neutral.

Substantive equality, by contrast, recognises that identical treatment can perpetuate or exacerbate disadvantage where groups start from unequal positions. It therefore permits—and often requires—differential treatment or positive accommodations to achieve genuine equality of outcome.

The CRPD Committee’s General Comment No. 6 on equality and non-discrimination explicitly calls on States Parties to:

“Ensure that reasonable accommodations and positive measures required to achieve substantive equality for persons with disabilities are provided in all areas, including education.” (GC 6, para 15)

2.2 UN CRPD Committee Jurisprudence

In J.D. v. United Kingdom (No. 22/2019), the Committee found that blanket policies which ignored disabled children’s individual needs violated Articles 5 and 24, because they failed to guarantee “inclusive education on an equal basis” and positive accommodations.

In K.M. v. Spain (No. 37/2019), the Committee emphasised that States must “eliminate discriminatory barriers” in access to education, including financial ones, recognizing that poverty and disability intersect to deepen exclusion.

2.3 ECHR’s Emerging Substantive Approach

Although traditionally more inclined to formal equality, the ECHR has in disability contexts moved towards substantive analysis:

In Autism–Europe v. France (27069/08), the Court held that failure to provide sign-language interpretation in public spaces breached Article 14 taken with Article 9 (freedom of expression), recognising the need for affirmative accommodations.

In Glor v. Switzerland (13444/04), the Court accepted that an apparently neutral tax measure could have a disproportionate impact on persons with disabilities, engaging Article 14’s requirement of objective and reasonable justification.

These precedents confirm that European human rights bodies do not view “equal tax treatment” as a shield against discrimination claims when the impact on a protected group is disparate and unjustified.

Agrandissement : Illustration 1

Agrandissement : Illustration 2

4. Applying CRPD Principles to the VAT Challenge

Respect for Inherent Dignity & Autonomy Clawing back support for families of disabled children by charging VAT denies parents the autonomy to choose the educational setting that best meets their child’s rights. CRPD Art. 3(a) demands that States uphold dignity by facilitating—not obstructing—those choices.

Non-Discrimination & Equality of Opportunity Disabled children without EHCPs—often from disadvantaged or minority backgrounds—are doubly penalised: first by lack of statutory recognition of their needs, and second by a regressive tax that falls heaviest on them. A substantive equality approach would mandate either a full exemption or a needs-based reduction in VAT.

Full & Effective Participation and Inclusion The VAT burden impedes schools’ ability to offer necessary accommodations—such as specialist therapists or resource rooms—because parents may reduce engagement when faced with higher fees. CRPD Art. 24(2)(c) requires States to ensure support measures that “facilitate effective education.”

Accessibility Financial accessibility is as critical as physical or communicational accessibility. A barrier that places education out of reach is incompatible with the CRPD’s holistic view of accessibility (Art. 9) and educational inclusion (Art. 24).

Respect for Evolving Capacities of Children By imposing VAT uniformly halfway through the school year, the policy ignores both children’s developmental needs and parents’ pre-existing financial commitments. The CRPD demands that States adopt policies that account for children’s evolving capacities (Art. 7).

Conclusion

Neidle’s tax-centric critique, while erudite in traditional ECHR and VAT doctrine, is blind to the lived realities of disabled children and their families. A proper, rights-based analysis—grounded in the CRPD’s human rights model and the evolving substantive equality jurisprudence of UN and European bodies—demands that the UK:

Exempt or reduce VAT on private school fees for children with disabilities lacking statutory support, so as to remove a discriminatory financial barrier.

Adopt positive measures across education and tax policy to fulfil its CRPD obligations of non-discrimination, accessibility and full inclusion.

Acknowledge the State’s positive obligations under both the CRPD and ECHR to ensure that tax does not erode fundamental rights, especially for society’s most vulnerable.

Far from a Pandora’s box, such targeted exemptions are a measured, proportionate and legally required step to achieve substantive equality and honour the UK’s commitments under international human rights law.

Ce blog est personnel, la rédaction n’est pas à l’origine de ses contenus.